GST is Goods and services tax which will substitute the old tax regime, where the ultimate tax burden and its cascading results will be lessened, with a concept of ONE INDIA ONE TAX.

Under this model there will be a single indirect tax, i.e GST which will substitute various indirect taxes levied on goods and services from manufacture till consumption.

Under this tax regime the concept of origin based taxation has changed to consumption based taxation (or destination principle).

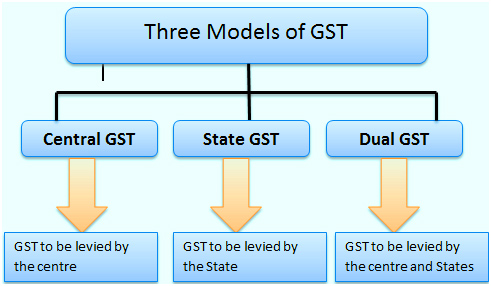

Federal structure of GST

Taxes will be subsumed as:

CGST – Central excise duty, Additional excise duty, service tax, CVD, Spl. Add. Duty @ 4%, surcharges and cess levied by central govt. Rates will be same across India.

SGST – Sales tax/VAT, Entertainment tax, luxury tax, taxes on lottery, betting & gambling, octori& entry tax, purchase tax, Surcharges &cess levied by state govt. Rates may vary for different states.

IGST – Taxes will be levied on interstate trade and taxes levied in the case of import. It will be sum total of CGST & SGST.

Legal Implications

The government of India is committed to replace all the indirect taxes levied in India with one tax GST, other than alcohol for human consumption.

Provisions will be made for removal of 650 check posts and 11 local taxes across India.

GST will be levied on sale of newspapers and advertisements.

Stamp duties imposed on legal documents by states will continue to be levied.

Petroleum and petroleum products may be subject to GST.

The list of exempted goods and services would be kept to minimum, it would be harmonised for the centre and state as far as possible.

GST is value addition at each level in the supply chain which will be applicable to both goods and services.

Where credit will be allowed for tax paid on input used in manufacture or for using any input service.

The Centre GST and State GST will be levied would be levied simultaneously on every transaction of supply of goods and services except on exempted goods and services, goods which are outside the purview of GST and the transactions which are below the prescribed threshold limits.

Input or input services for personal consumption will continue to be GST regime.

An additional 1% tax will be levied by the centre which will be redirected to origin states for a period of 2 yrs or more as may be proposed by the central govt.

GST Impact on Sectors/Companies in a Nutshell

Banks – Current Tax Rate is 15%. After GST it is 18%. Negative

Consumer Staples – Current Tax Rate is 22%. After GST it is 18%. Positive for Asian Paints, Dabur, HUL, Emami; Negative for ITC, UBL

Consumer Discretionary – Current Tax Rate is 15%. After GST it is 18%. Negative for Jubilant Foods, Cafe Coffee Day, Restaurant businesses

Media & Entertainment – Current Tax Rate 15% + 7% State Entertainment tax. After GST it is 18%. Positive for Dish TV, Videocon D2H, BIG TV

Telecom – Current Tax Rate is 15%. After GST it is 18%. May see marginal dip in consumption

Auto & Auto Ancillary – Current Tax Rate is 27%. After GST it is 18%. Positive for M&M, Maruti, Bajaj Auto, Eicher Motors, Ashok Leyland

Metals – Current Tax Rate is 18%. After GST it is 18%. No significant impact.

Cement – Current Tax Rate is 27%. After GST it is 18%. Positive for UltraTech, Shree Cement, Ambuja Cement

Pharma – Current Tax Rate is 15%. After GST it is 18%. Negative for Pharmaceutical co.s

Real Estate – Current Stamp Duty is 15%. After GST it is 16%. No significant impact.

Logistics – No change in Tax Rate after GST. Positive for Container Corp, GATI, etc.

Scheme of levy

The Levy in the common parlance means charge or imposition or collection of tax by authority. For the purpose of collection of tax, the authority should have the power of collection of tax.

Section 7 of Model GST Act 2016, sets out that CGST/SGST and IGST shall be levied on all intra-state sales and interstate supplies of goods and/or services.

The Assessee who has an aggregate income of Rs. 50 lakh are eligible for composition levy, where amount of tax payable is 1% of the turnover during the year where the assesse shall not be entitled to claim any input tax credit.

Under the GST regime the threshold limit for SME’s is proposed to be around Rs. 25 Lakh. The lowering of the threshold would bring many SME’s under the Tax bracket.

GST Model law has also brought supply of goods or services without consideration, under the tax bracket, by imposing tax on value derived under Rule 4 of valuation rules.

Under section 43C(4) of Model GST Law, states that every e-commerce operator shall furnish a statement

electronically, providing the details of the amount collected on behalf of each supplier in respect of all supplies of goods and/or services effected through the operator.

Imported goods would be liable to custom duty along with IGST (equivalent to IGST on similar goods in India).

Utilisation of Input credit

Chapter-V states that Every taxable person shall, subject to such conditions and restrictions as may be prescribed in this behalf, be entitled to take credit of input tax and may deduct the amount of admissible credit in respect of a tax period from the output tax for the same period and pay the remaining amount, if any, to the credit of the appropriate Government (i.e. Central Government in case of the IGST and the CGST, and the State Government in case of the SGST) within such time and in such manner, as may be prescribed.

Manner of taking credit of IGST/CGST/SGST:

IGST paid on interstate purchase shall first be utilised towards payment of IGST then (if amount remaining) towards payment of CGST and SGST, respectively.

CGST paid on purchase shall first be utilised towards payment of CGST then (if amount remaining) towards payment of IGST.

SGST paid on purchase shall first be utilised towards payment of SGST then (if amount remaining) towards payment of IGST.

ITC of CGST cannot be utilised towards payment of SGST.

ITC of SGST cannot be utilised towards payment of CGST.

There shall be two type of electronic ledgers for every registered taxable person:-

Electronic Cash Ledger

Electronic Credit Ledger

Every deposit made towards tax, interest, penalty, fee or any other amount shall be credited to his Electronic Cash Ledger.

Input Tax Credit as self-assessed in the return shall be credited to his Electronic Credit Ledger. The amount available in this ledger may be used for making any payment towards tax payable under GST Law.

Procedural Aspects

New Applicant can apply for Registration:

At the GST Common Portal directly ; or

At the GST Common Portal through the Facilitation Center (FC)

As per the following process:

Constitution of Business –

Partnership Deed in case of Partnership Firm ;

Registration Certificate in case of other businesses like Society, Trust etc. which are not captured in PAN.

In case of Companies, GSTN would strive for online verification of Company Identification Number (CIN) from MCA21. Constitution of business / applicant as per PAN would be taken except for businesses such as Society, Trust etc. which are not captured in PAN. Partnership Deed would be required to be submitted in case of Partnership Firms.

Details of the Principal Place of business –

In case of Own premises – any document in support of the ownership of the premises like Latest Tax Paid Receipt or Municipal Khata copy or Electricity Bill copy.

In case of Rented or Leased premises – a copy of the valid Rent / Lease Agreement with any document in support of the ownership of the premises of the Lessor like Latest Tax Paid Receipt or Municipal Khata copy or Electricity Bill copy

In case of premises obtained from others, other than by way of Lease or Rent – a copy of the Consent Letter with any document in support of the ownership of the premises of the Consenter like Municipal Khata copy or Electricity Bill copy

Customer ID or account ID of the owner of the property in the record of electricity providing company, wherever available should be sought for address verification

This is required as an evidence to show possession of business premises. If the documentary evidence in Rent Agreement or Consent letter shows that the Lessor is different from that shown in the document produced in support of the ownership of the property, then the case must be flagged as a “RiskCase”, warranting a post registration visit for verification. GST Law Drafting Committee may add penalty provision for providing wrong lease details.

Details of Bank Account(S) Opening page of the Bank Passbook held in the name of the Proprietor / Business Concern – containing the Account No., Name of the Account Holder, MICR and IFS Codes and Branch details This is required for all the bank accounts through which the taxpayer would be conducting business.

Details of Authorised Signatory For each Authorized Signatory:

Letter of Authorisation or copy of Resolution of the Managing Committee or Board of Directors to that effect This is required to verify whether the person signing as Authorised Signatory is duly empowered to do so.

Benefits of GST

This structure would overall reduce the combined rate of taxation and the cascading burden on the economy.

This would increase the productivity and performance in the economy.

Indian truck system will work effectively with removal of 650 check posts and 11 local taxes.

Reduction of cost to the company for extra working capital.

Reduction in typicality of existing tax structure in India.

A transparent and simple tax regime of ONE TAX ONE INDIA.

Limitations under GST Model

When the aviation industry was witnessing the much awaited growth with increasing domestic traffic, the GST implementation might slower the rate at which the industry is expecting growth as flying will become expensive.

India, on one hand, has the lowest insurance penetration in the world (less than 5% of Indian population & half of the global average) and on the other GST will further make the insurance products dearer.

The Banking & Financial Sector (including Insurance as statedabove) might take a hit as currently the effective tax rate in the sector is 14 per cent, which is levied only on fee component (and not interest) of the transaction. Under GST, effective tax rate on fee-based transactions is expected to increase to 18-20%.

Petroleum products form a majority import value in the Indian ecosystem. However, key petroleum products like crude, natural gas, high-speed diesel and ATF have been kept out of GST.

Conclusion

A seamless implementation of GST may boost growth of the overall economy to a level that the above stated pitfalls might be merely seem as part and parcel of the India growth story. When most of the sectors grow simultaneously, it might increase jobs and disposable income of individuals to an extent that the dearness brought by GST gets offset. Analysts are already predicting 10% GDP growth for the Indian Economy with GST coming into effect.